Chapter 7

Corporations: The Financial Statements

367

Analysis

In this chapter, you have learned how to calculate earnings per share. Often, a corporation’s

annual report will report earnings per share as calculated by the corporation. Rarely do the

corporation’s reported earnings per share agree with a financial analyst’s calculation of this

number. Discuss why these two calculations may differ.

AP-13B

(

6

)

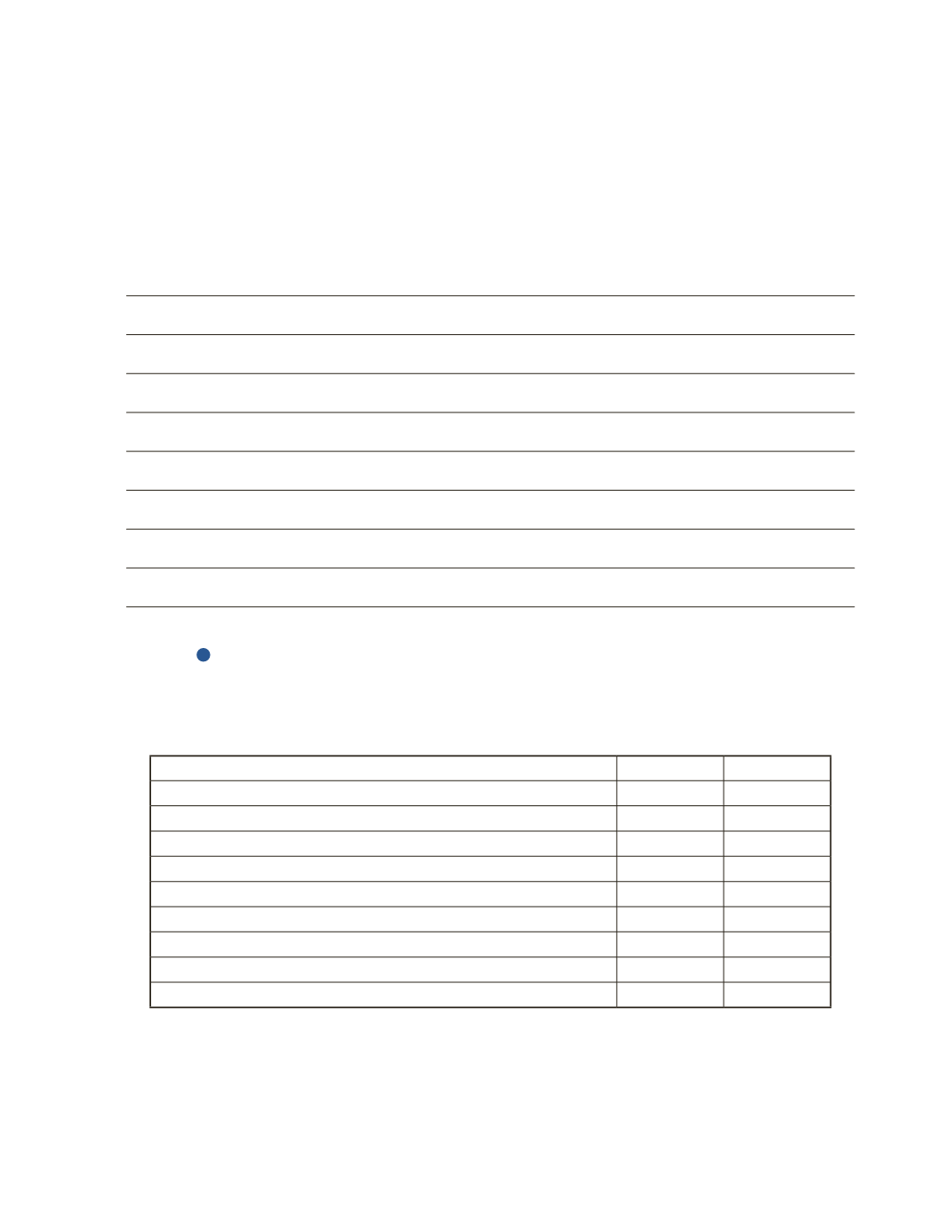

Marry Inc. provided the following information from its accounting records for the years

ending December 31, 2017 and 2016.

2014

2013

Income from continuing operations (net of tax)

$840,000

$740,000

Income from discontinued operations (net of tax)

150,000

70,000

Net income

990,000

810,000

Each year, 100,000 common shares were outstanding

1,000,000

1,000,000

Beginning retained earnings

1,990,000

1,580,000

Current liabilities

560,000

420,000

Non-current debt

980,000

760,000

Market price per share

15

13

Total dividends paid

500,000

400,000

No shares were issued or redeemed during the two years. The company has never issued any

preferred shares.

Required

Calculate the following ratios for both years.