Chapter 8

Non-Current Liabilities

428

Case Study

CS-1 (

1

7

)

You & Us Company issued a callable six-year, $1,000,000 bond on December 1, 2013. The

interest rate was 4% per year and interest payment would be made semi-annually. In 2013,

similar bonds were paying 6% interest on average.

On December 1, 2016, the average market interest rate for similar bonds had decreased to

2%. You & Us Company decided to redeem all the outstanding bonds issued in 2013 and issue

new bonds. The new bonds will also have an annual interest rate of 4%. You & Us Company’s

fiscal year-end is on December 31.

In 2013, You & Us Company hired a bookkeeper, who did not have a professional accounting

designation. The bookkeeper recorded the journal entries for the issuance of the bond and

the two payments of interest in 2014, which are all shown below.

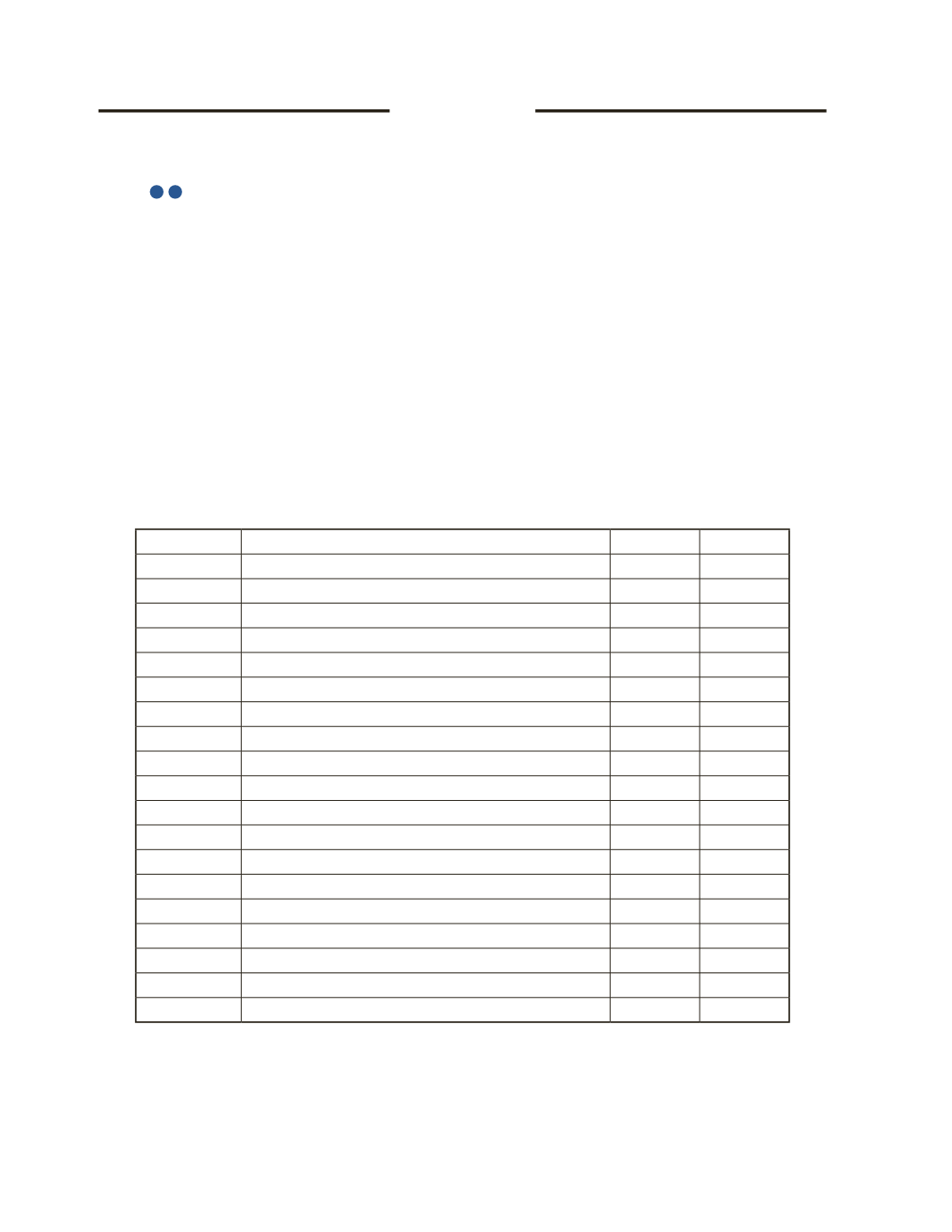

Date

Account Titles and Explanations

Debit

Credit

Dec 1, 2013 Cash

900,480

Discount on Bonds

99,520

Bonds Payable

1,000,000

To record issuing of $1,000,000 bonds at discount

Dec 31, 2013 No journal entry on issued bonds

Jun 1, 2014 Interest Expense

20,000

Cash

20,000

To record interest payment on bonds

Dec 1, 2014 Interest Expense

20,000

Cash

20,000

Record interest payment on bonds

Dec 31, 2014 No journal entry on issued bonds