Chapter 9

Investments

475

Case Study

CS-1 (

2

)

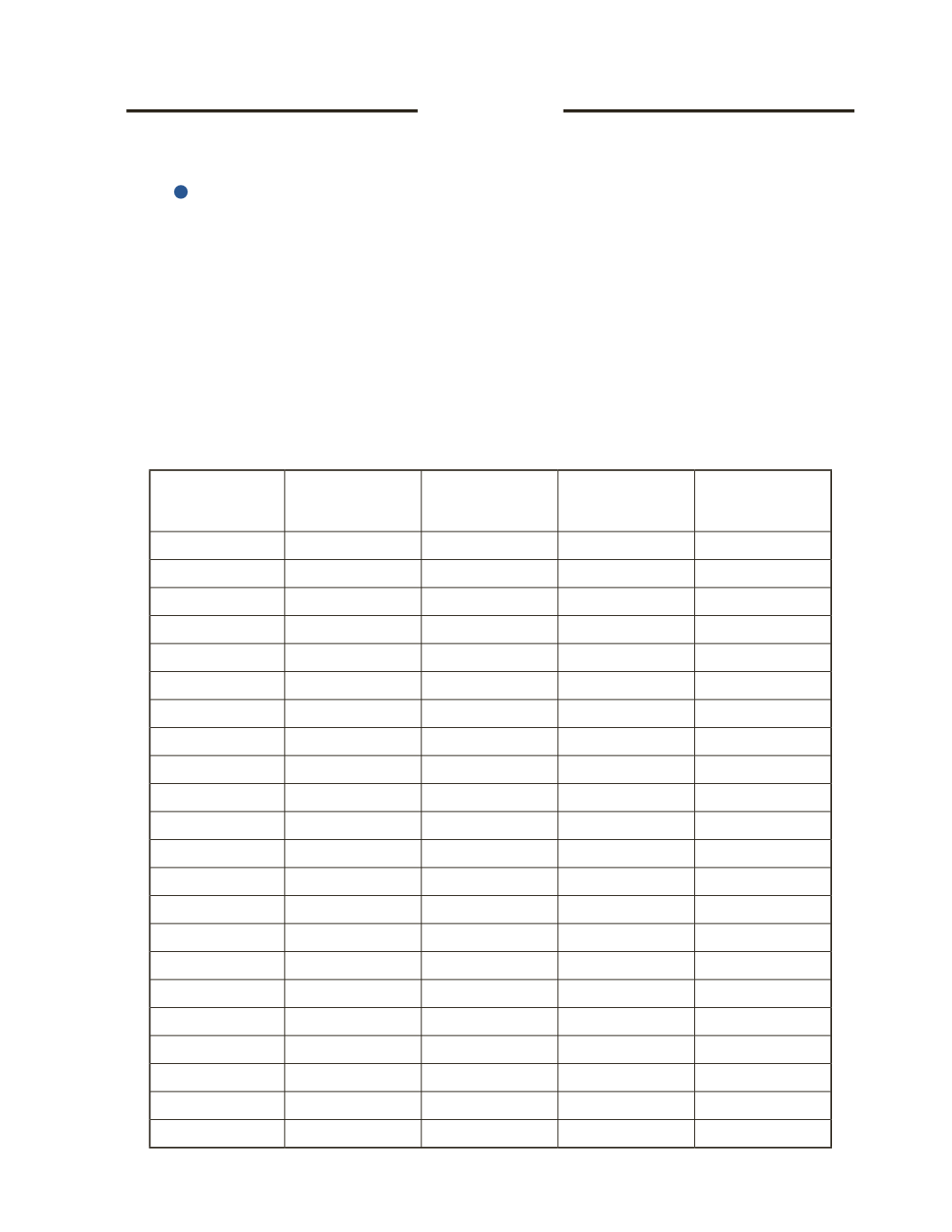

A five-year bond of $500,000 was issued on March 1, 2016 with the coupon rate of 6%. The

market interest rate was 4% at that time. Interests are paid semi-annually on March 1 and

September 1 every year. Both the issuer and the investor have a year-end date on December

31. Assume both the investor and issuer follow IFRS.

Required

a) Using the Present Value Factors, prepare an amortization table from the issuance date to

maturity.

Interest Period

A

Interest Payment

B

Interest

Expense/Revenue

C

Premium

Amortization

D

Bond

Amortized Cost